E-mail: send me e-mail!

E-mail: send me e-mail! This page is dedicated to the readers´ contributions about real options approach. Contributions don't need be petroleum specific.

Are welcome materials like working papers, abstracts, dissertations, comments of papers, multimedia materials, book reviews, spreadsheets, software in general, and so on.

If you wish to publish some material, don't hesitate:

E-mail: send me e-mail!

Note on Downloads: in many times you will need to download a

compressed (zip) file. In these cases you need to use a decompressing

software (like zip-it, winzip, pkunzip, etc.). You could get these

compression software at Nico Mak

Computing for Winzip, at

Vertisoft for Zip-it, and at Pkware for

PKZip. For paper files in a Word (.doc) or Presentation in

Powerpoint (.ppt), you can need of the freeware Viewers Software (you can

see the file and print, but not to change) at the

Microsoft site.

For Adobe Acrobat files (.pdf), go to the

Adobe Acrobat Website.

![]()

The first contribution comes from Europe. The Ph.D. Giovanni Beliossi, from London Business School, and also lecturer in Finance at the Universitá di Bologna. He is also Associate of Real Options Group.

This paper was presented at the FMA conference, in October 12, 1996, in New Orleans (USA). At this time Beliossi was a Ph.D. candidate.

You can send an e-mail to Giovanni

Beliossi: g.bel@europe.com

![]() See also:

Comments from the editor of this site!

See also:

Comments from the editor of this site!

Note: If you want comment all the paper or some topic (to publish in this

site), send me an e-mail.

Download the paper: you will get the compressed (zip) file. The working paper file after decompression has a Word 6.0 format.

![]() File las_fma3.zip with 52,349 bytes (compressed version).

File las_fma3.zip with 52,349 bytes (compressed version).

We propose the idea that the best way to assess the value of a properly managed portfolio of operating options is to price them as a portfolio of financial options with the same features. Thus the best way to appraise the full profit potential of a company whose assets consist of operating options is to price it via option pricing theory. Consequently, a positive difference between the option pricing value and a passive NPV value of an oil firm, or its market value should explain at least some of the unexploited value of management. We build on this point empirically and assess the value of the assets of Lasmo, a British oil firm, just before the firm is subject to a hostile take-over bid, pricing its undeveloped reserves as a portfolio of options. Corporate financial theory suggest that take-overs are disciplinary devices whose targets are firm with inefficient management. We find that our option pricing value of Lasmo actually exceeds the contemporaneous market capitalisation of the firm. We interpret this positive difference (+5%) as consistent with the presence of managerial inefficiencies.

By M.Sc. Marco A.G. Dias

The working paper of Giovanni Beliossi is very interesting. He uses

option approach to detect managerial inefficiencies in an UK oil company,

and so justify the hostile take-over of Lasmo at the beginning of 1994. He

valuates the Lasmo assets, and the idea is: "as a first

approximation, option pricing of an oil company's assets includes the

value of efficient management, while traditional NPV does not".

Comparing this valuation with the Lasmo's market value, is possible to

find managerial inefficiencies.

The proved reserve valuation is very known (see for example Dixit & Pindyck, chapter 12): the proved undeveloped reserve is like a call option on a developed reserve, whose strike price is the development cost (investment to get the production).

One of more interesting contributions of this paper is the probable

undeveloped reserves valuation method. In order to transform a probable

reserve into a proved reserve, it is necessary to spend the exploration

investments (to gather information), usually by drilling new wells and/or

by seismic methods. So, a probable reserve is like a call option on a

proved undeveloped reserve, whose strike price is the cost of exploring

the field. The underlying asset is the option to develop the field. So,

there is a compound options problem.

In this method, the crucial step is the dividend yield (or convenience

yield) estimation. In the case of developed reserve, this parameter is the

cash flow yield; in the case of oil barrel, this parameter is estimated

from futures market for oil prices. In both cases the estimation is very

easy.

However, for the undeveloped proved reserve, someone can argues that the

dividend is zero. But this question is not so simple: the reduction of the

uncertainty due to the exploration investment can be seen as a "shadow"

dividend.

Unfortunately, the author doesn't present (at least in this version of

paper ) how was estimated this important parameter. He argues: "Solving

these theoretical and empirical issues is the subject of our current

research on the topic".

Thinking information value like dividends is perhaps an innovative

approach.

Probably is not possible to imagine a continuous dividend, but perhaps a

discrete dividend sounds feasible. If you think exploration as a

sequential discrete investments, there are the corresponding discrete

shadow dividends. The differential equation must be adapted in this case

of discrete dividend.

I think the possible advantage of this method is practical: the analogy

with financial options (American call) on stocks with discrete dividends.

The technical uncertainty effect is captured by the discrete dividend, so

there is early exercise of the option to be calculated.

The more rigorous approach for this case is the alternative method of

Dixit & Pindyck (chapter 10, section 4) adapted for this case. The

approach consider both, technical and economic uncertainties in the same

variable (in the book is the cost, in our case is the revenue). The

investment is also sequential and with technical uncertainty reduction

(creating a shadow value). The difference of the case with

technical uncertainty and without technical uncertainty, perhaps

brings some indication about the dividend for the working paper approach.

I think that, in the adapted model of Dixit & Pindyck, there is

dividend yield only for the developed reserve. The dividend yield for

undeveloped reserve is zero.

However, the Beliossi's idea may reach a good theoretical consistency and

perhaps some practical advantage over the alternative rigorous method.

These ideas are very interesting, and is necessary further research. What

do you think about, reader?

There are many other ideas in the paper, such as this instructive

insight: "option pricing allows to price future options on tradable

assets when they are exercised optimally even without knowing how

they are going to be optimally exercised in the future"

In short, the Giovanni Beliossi's paper is very important, and presents

challenging features.

By Ph.D. Arun Muralidhar, from MIT.

Dr. Arun Muralidhar presents part of his Doctoral Dissertation, at Sloan

School of Management, MIT.

He shows how the global uncertainties (co-variations of countries) in tax

rates, exchange rates, input costs (like wages), etc., add real options

value for a multinational enterprise (MNE), due its additional financial

and operational flexibility. Some projects can be acceptable for MNEs, but

not for national firms without the same options.

Go to the special Dr. Muralidhar Contribution Webpage, with abstracts, two papers to download (chapters from his dissertation), and see some special highlights that I selected from this very important research.

You can send an e-mail to Dr. Arun

Muralidhar:

arunmura@hotmail.com.

("Avaliação de Investimento de Capital em Projetos de Geração Termoelétrica no Setor Elétrico Brasileiro Usando Teoria das Opções Reais").

By M.Sc. Alessandro Lima de Castro, PUC-Rio and CEPEL

See the abstract below (in English) and download both dissertation and the presentation of the dissertation (in Portuguese).

In the Brazilian Electric System about 92% of the generated electricity is of hydraulic origin. Today the system is operating practically in the limit of your capacity. Solutions of short time to make possible the expansion of the offer of electricity generation go by the installation of cycle combining thermal using natural gas as fuel. In this Dissertation, I use the Real Options Theory to evaluate generation assets in the Brazilian Electricity Sector. In the Brazil, central operator dispatches a flexible thermal when the electricity spot price is larger than the operation costs. The operation decision is like an European call, where underlying asset is the electricity and the strike price is the operation cost. The value of the capacity is the sum of all decisions to operate the thermal unit, in the remaining life of unit. I use Monte Carlo Simulation and Dynamic Programming to evaluate this model. The problem is divided in two parts. In the first part, the base case is fixed and evaluated. The expected NPV and Project Risk are calculated in function of contract level. In the second part, many sensibilities are done in relation to base case. At the end, the value of flexibility is calculated, for each contract level.

![]() Download the

pdf file (Adobe Acrobat) of the M.Sc. dissertation (in Portuguese):

Alessandro-Dissertacao_Mestrado.pdf, with 481 KB.

Download the

pdf file (Adobe Acrobat) of the M.Sc. dissertation (in Portuguese):

Alessandro-Dissertacao_Mestrado.pdf, with 481 KB.

![]() Download also

the pdf file (Adobe Acrobat) of the M.Sc. dissertation presentation (in

Portuguese):

Alessandro-Dissertacao_Apresentacao.pdf, with 952 KB.

Download also

the pdf file (Adobe Acrobat) of the M.Sc. dissertation presentation (in

Portuguese):

Alessandro-Dissertacao_Apresentacao.pdf, with 952 KB.

You can send an e-mail to M.Sc.

Alessandro Castro:

aleslima@yahoo.com.

Master's Thesis in Financial Economics

By M.Sc. Charlie Grafström & MSc. Leo Lundquist, from Stockholm

University - School of Business. Tutored by Professor Lars Vinell.

See the abstract below and download the dissertation (in English).

We examine whether the value of an undeveloped oilfield is affected by

using real option valuation. Applying a two-factor model dependent on the

spot price of Brent and the convenience yield implies a premium over the

certainty equivalent method ranging from 20-1000%, for reasonable spot

prices.

However, the premium over the risk-adjusted method can be negligible since

values are dependent on the spot price forecasts of managers. This does

not mean that the option criterion should be neglected, considering its

implications for the strategic decision of when to optimally invest.

The risk-adjusted approach suggests that investment is optimal whenever

oil prices surpass $15.69 per barrel, whereas the real option analysis

suggests production at prices above $26.72.

Moreover, we find evidence of a positive market price of convenience yield

risk on the IPE, strongly disagreeing with economic theory.

![]() Download the

pdf file (Adobe Acrobat) of the M.Sc. dissertation:

charlie-leo-dissertation.pdf, with

448 KB.

Download the

pdf file (Adobe Acrobat) of the M.Sc. dissertation:

charlie-leo-dissertation.pdf, with

448 KB.

You can send an e-mail to MSc. Leo

Lundquist:

leo.lundquist@spray.se.

("Um Estudo Sobre a Teoria das Opções Reais Aplicada à Análise de Investimentos em Projetos de Pesquisa e Desenvolvimento (P&D)").

Master's Thesis in Production Engineering

By M.Sc. Elieber Mateus dos Santos, from Universidade Federal de

Itajubá (Minas Gerais, Brazil). Advised by

Professor Edson de

Oliveira Pamplona.

See the abstract below (in English) and download the dissertation (in Portuguese).

The competitive environment in which enterprises are involved has created a need for them to be able to adapt to change quickly. Companies can achieve this by investing in projects which create options for the companies, instead of "killing" them. This can provide the companies with flexibility which is a valuable tool that can make a difference. For this reason, the use of traditional techniques of investment analysis, mainly the Discounted Cash Flow (DCF, has been severely criticized because it has not been able to capture the "management flexibility" value. This fact has led practioners and academics to search for sophisticated methods of investment analysis which are able to treat uncertainty, irreversibility, and learning.

The option pricing theory's ability to quantify the investment's flexibility in strategic projects makes it an attractive choice when compared to the standardized analysis made through DCF. The incorporation of this flexibility can increase the project's total value and its possibility of being accepted, and this is an incentive for using it in practice. The value of a project's flexibility is basically a real options collection whose price can be calculated using the known financial option techniques. Despite being in a development and establishement process, the Real Options Theory (ROT) raises a promising "option" to treat these factors because it is able to be applied to several fields.

The present work focuses mainly on Real Options Theory applied to investment analysis in Research and Development (R&D) projects. The dissertation also provides empirical evidence of the underlying power of the theory. This is accomplished by the application of the methodology to assess a real R&D project. This also will contribute in the reduction of the gap between theory and practice. Two methods are used: the Kallberg and Laurin (1997) model and the Geske (1979) model, adapted to real options by Kemna (1993) and pointed by Perlitz, Peske and Schrank (1999) as a good tool to assess compound options. The results of the application are compared with those obtained through the traditional DCF and decision tree. In conclusion the Real Option Theory, although it seems more complex, it can be used as an important and promising tool, helping managers to think clearly and strategically in a decision making process.

![]() Download the

compressed (.zip) Word for Windows file of the M.Sc. dissertation:

elieber_dissertation.zip file with 281

KB (in Portuguese).

Download the

compressed (.zip) Word for Windows file of the M.Sc. dissertation:

elieber_dissertation.zip file with 281

KB (in Portuguese).

You can send an e-mail to MSc. Elieber

Mateus dos Santos:

eliebersantos@yahoo.com.br.

("Validação do Critério de Avaliação de Projetos Utilizando a Teoria das Opções Reais: E&P de Campos de Petróleo Nacionais, Supondo Pre�os como Movimento Geom�trico Browniano").

Master's Thesis in Production Engineering

By M.Sc. Viktor Nigri Moszkowicz, PUC-Rio, Dept. of Industrial Engineering, Rio de Janeiro, Brazil. Advised by Professor José Paulo Teixeira.

See the abstract below (in English) and download the dissertation (in Portuguese).

Financial researchers have discussed a lot about the theoretical advantages of including the managerial flexibility and the financial options analogy in projects valuation criteria. Plenty of authors criticize the currently used investment analysis methods, mainly represented by the discounted cash flow, supported by the notion that the managers should use techniques that better reflect the available flexibility to take their decisions. In this sense, the present dissertation has the objective of validating the suggested advantages of using the Real Options theory through a back-testing focused on oil fields with Brazilian oil industry representative characteristics. Those tests will be carried out for the 1970-1990 period, considering the economic uncertainty and excluding the technical uncertainties.

The investment decisions model developed in Excel and VBA (Visual Basic for Applications) contemplates the options of waiting till two years and of choosing among three exploitation intensities. The Geometric Brownian Motion was assumed as the stochastic process to represent the real oil prices time evolution, and its volatility was varied to generate a sensibility analysis. Finally it is worthy to state that the results shall not be accepted as definitive, and just as a foundation to future studies on the empirical research line of verifying and validating the theoretical advantages of the Real Options with regard to others currently used criteria.

Keywords: Investment analysis, project valuation, real options, oilfields, back-testing, geometric Brownian motion, investment under uncertainty.

![]() Download the three Adobe Acrobat (.pdf) files of the M.Sc. dissertation (in Portuguese):

Download the three Adobe Acrobat (.pdf) files of the M.Sc. dissertation (in Portuguese):

tese_viktor-01165032-pretextual.pdf file with 189 KB.

tese_viktor-01165032-corpo.pdf file with 1246 KB.

tese_viktor-01165032-postextual.pdf file with 1870 KB.

You can send an e-mail to MSc. Viktor Nigri Moszkowicz: viktor.nigri@cvrd.com.br.

("Contribuições da Abordagem de Avaliação de Opções Reais em Ambientes Econômicos de Grande Volatilidade - Uma Ênfase no Cenário Latino-Americano").

Master's Thesis in Controlling and Accountancy

By M.Sc. Regina Caspari Monteiro, USP (Universidade de São Paulo), Faculty of Economics, Administration, and Accountancy, São Paulo, Brazil. Advised by Professor Alexandre Assaf Neto.

See the abstract below (in English) and download the dissertation (in Portuguese).

In corporate finance and traditional capital budgeting, discounted cash flow methods have prevailed as the basic structure in most approaches to investment and shareholder value analysis. The evolution of the option pricing theory, however, has added a whole new set of tools to the traditional group of theories and practices, necessary to the good management and exploitation of the value from uncertainty and volatility. These tools broaden the value generation parameters by adding the managerial flexibility and uncertainty concepts. Amid this overall context, the present work has tried to research and present the real asset investment analysis methodology based on the option pricing theory (real options), its characteristics, limitations and applications in business environments characterized by high economic volatility.

Therefore, this study begins with the review of several theories used in capital budgeting, aiming to present them from their most basic form, up to the main, most sophisticated and recent methods, which include concepts like time value of the money and risk. Finally, in order to demonstrate the applicability of the methods discussed, a theoretical exercise, which simulates a real case, is developed, considering an environment of high volatility, analyzing the opportunities that the real options theory may grant. As a result of this study, it is concluded that the real options analysis may be a viable and preferable alternative if compared to traditional methodologies, when used in an uncertain environment, in association with managerial flexibility, like the general environment that characterizes the Latin America region.

![]() Download the Adobe Acrobat (.pdf) file of the M.Sc. dissertation (in Portuguese):

Download the Adobe Acrobat (.pdf) file of the M.Sc. dissertation (in Portuguese):

regina-dissertacao-defesa.pdf file with 943 KB.

You can send an e-mail to MSc. Regina Caspari Monteiro:

rcmontei@uol.com.br.

![]()

By D.Sc. Jerry P. Flatto

You can send an e-mail to Jerry P.

Flatto: JFlatto@sprynet.com

, who do research on real options applied to information

technology.

Go to the online paper "Using Real Options in Project Evaluation"

By M.Sc. Katia M.C. Rocha, Institute for Applied Economic Research - IPEA - from Brazilian Government.

Katia presents an overview of numerical techniques that has been used in the real options practice. She describes with more details the finite differences method.

Go to the online article Numerical Techniques for Real Options, by Katia Rocha.

You can send an e-mail to M.Sc. Katia

Rocha: katiaroc@iis.com.br.

In a future article, Katia will analyze with more details, the methods

for American options evaluation using Monte Carlo simulation (see also the

Dias paper on Monte Carlo for real options in this website).

One important advantage of Monte Carlo simulation is the computation time

that grows linearly in the number of state variables, not exponentially.

Lattice methods like the popular binomial, although very useful to develop

the intuition, have the drawback that computing time grows exponentially

in the number of state variables.

Bachelor's Thesis from the Dalarna University (Sweden), by Håkan Jankensgård.

Thanks to the Thesis Examinator, Professor Lars Hultkrantz, who oriented Jankensgård and let me know this very interesting and comprehensive option-game dissertation.

See below an excerpt from this dissertation (item 1.3 - Purpose), and download the entire monograph (both in English).

Purpose: In this essay I propose a way to model the opportunity cost of waiting using game theory that can be integrated into the binomial model for options pricing. My hypothesis is that the opportunity cost can be derived from seeing the capital investment as a game of incomplete information, and that this cost can in turn be modeled in much the same way dividends are modeled in options pricing.

![]() Download the

monograph: the Word for Windows file (.doc): the-option_game-to-defer-nya.doc,

with 404 Kb.

Download the

monograph: the Word for Windows file (.doc): the-option_game-to-defer-nya.doc,

with 404 Kb.

Or download the compressed version: the-option_game-to-defer-nya.zip, file with 85 Kb.

You can send an e-mail to Håkan

Jankensgård:

hakanjankensgard@hotmail.com.

By D.Sc. Luiz Eduardo Brandão, from PUC-Rio.

The instructor's manual (in Portuguese) covers the chapters 2 to 8 of the classic Dixit & Pindyck textbook Investment under Uncertainty.

In this manual the readers will find the translation of the chapters to Portuguese, many proofs not developed by the authors, and additional discussion of many points for better understanding. It is a must for students and teachers using this classic book.

![]() To download the

compressed .pdf files for the

chapters 2 and 3 (file dp_disclaimer-chapters2_3.zip with 852

KB).

To download the

compressed .pdf files for the

chapters 2 and 3 (file dp_disclaimer-chapters2_3.zip with 852

KB).

![]() To download the

compressed .pdf files for the chapters 4

and 5 (file dp_chapters4_5.zip with 743 KB).

To download the

compressed .pdf files for the chapters 4

and 5 (file dp_chapters4_5.zip with 743 KB).

![]() To download the

compressed .pdf files for the chapters 6

and 7 (file dp_disclaimer-chapters6_7.zip with 441 KB).

To download the

compressed .pdf files for the chapters 6

and 7 (file dp_disclaimer-chapters6_7.zip with 441 KB).

![]() To download the

compressed .pdf files for the chapter 8 (file

dp_chapter8.zip with 876 KB).

To download the

compressed .pdf files for the chapter 8 (file

dp_chapter8.zip with 876 KB).

Disclaimer by Luiz Eduardo Brandão:

This manual is a compilation of the class notes of Prof. Tara Baidya for the course "Advanced Topics in Corporate Finance (IND 2078)" at the Industrial Engineering Department of the Pontifical Catholic University of Rio de Janeiro during the academic years of 1988, 1999 and 2000. This work also benefited greatly from the contribution of the graduate students Alessando Castro (Chapter 3), Maria de Fátima Pombal and Eliane Thompson-Flôres (Chapter 8), and José Carlos Abreu (Chapters 2 to 6). The final responsibility for the editing, compilation, revision and organization of the work is mine, as well as of any errors in it. Luiz Eduardo Brandão, July/2000.

You can send an e-mail to the doctoral

candidate Luiz Eduardo Brandão: Luiz.Brandao@bus.utexas.edu

.

The Matlab files - available to download, are offered for educational purposes only, by Luke J. Sparvero, Senior Lecturer in Finance and Real Estate from University of Texas at Arlington.

The user must have Matlab's optimization toolbox to run the programs. Any text editor can read these files.

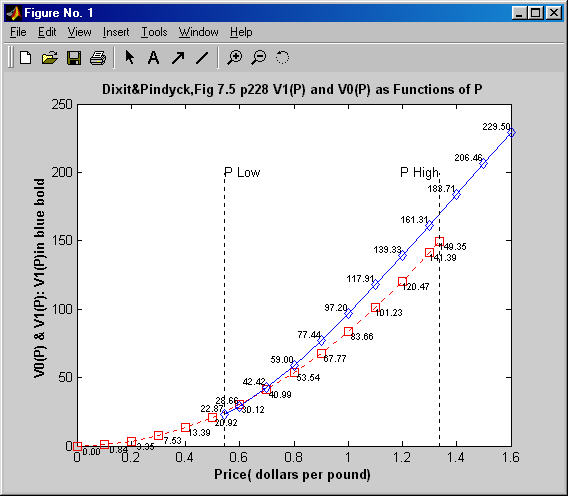

Below are listed the Matlab files as well as the correspondent figure in the Dixit & Pindyck's book. In both cases there are links to download the Matlab and the image files.

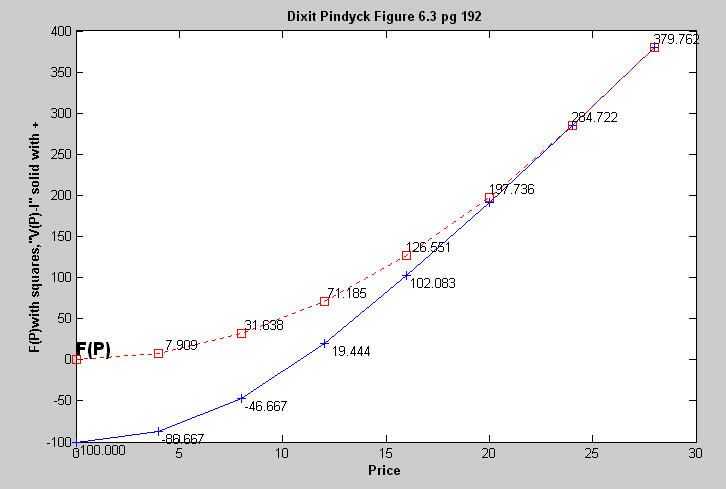

![]() Download the Matlab file

dpfigure63.m, for the Figure 6.3 from Dixit & Pindyck textbook

(file dpfigure63.m with 6 KB).

Download the Matlab file

dpfigure63.m, for the Figure 6.3 from Dixit & Pindyck textbook

(file dpfigure63.m with 6 KB).

See the correspondent figure by clicking here (file dpfigure6_3 p192.jpg with 27 KB).

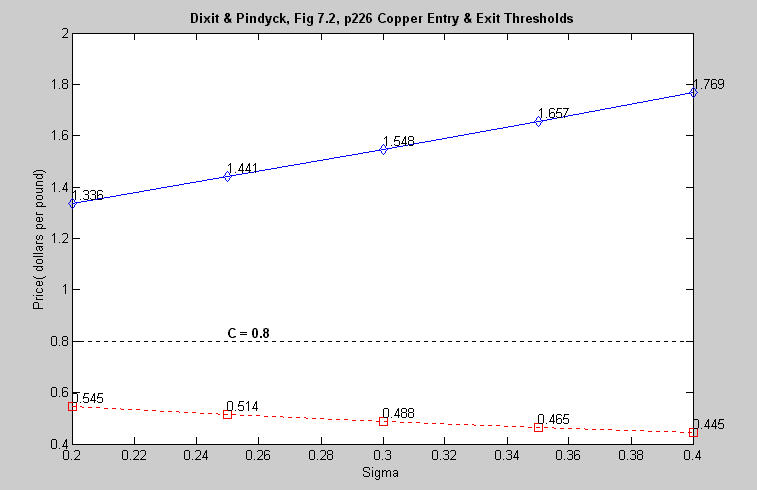

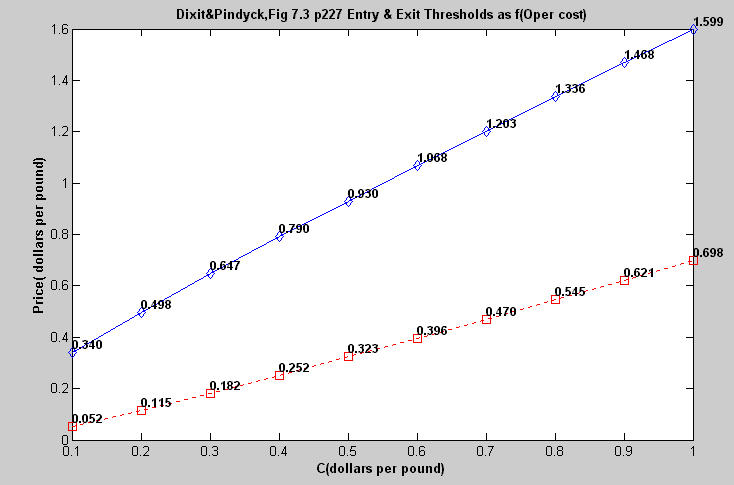

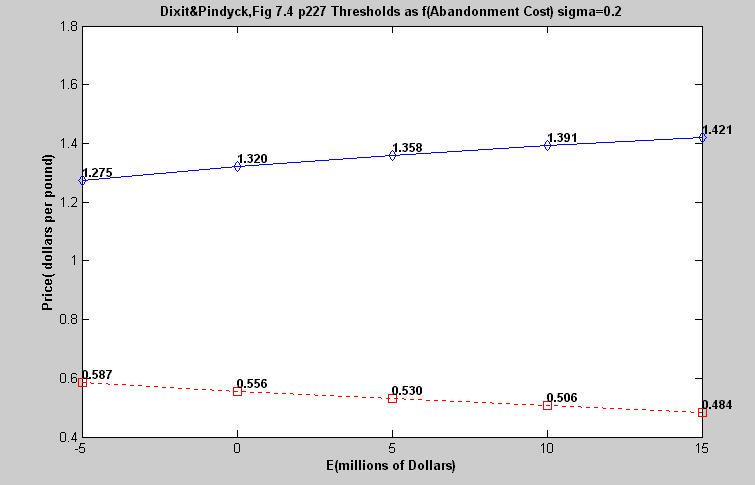

![]() Download the Matlab files from Dixit & Pindyck textbook, chapter 7:

Download the Matlab files from Dixit & Pindyck textbook, chapter 7:

You can send an e-mail to Luke J. Sparvero lsparver@exchange.uta.edu.

.

Bachelor's Thesis from Stockholm University, Department of Economics, Sweden, by M.Sc. Leo Lundquist, Spring 2003. Tutored by Professor Mats Persson.

This very interesting monograph on bids in offshore leases at GoM (Golf of Mexico) discusses topics like "winner's curse" and value of option, presenting econometric tests that support the option pricing theory. Matlab code used in the monograph is available at the dissertation appendix. See below the abstract and download the entire monograph (both in English).

I examine whether a two-factor real option model, dependent on the spot price of crude oil and the convenience yield, can explain the highest bids in offshore petroleum auctions held by the U.S. Government. Applying the model to 23 viable offshore leases, offered in the Federal lease sale No. 178 part 1, suggests that the option model is successful in justifying the high bids. Sample mean option values are more than three times larger than the average high bids, which strongly contradicts the notion of a winner�s curse in offshore petroleum auctions. Moreover, evidence is presented indicating disparities between the short- and long-term market price of convenience yield risk for crude oil futures on NYMEX.

![]() Download the

monograph in Adobe Acrobat (.pdf) file: lundquist_nekupps.pdf,

with 251 Kb.

Download the

monograph in Adobe Acrobat (.pdf) file: lundquist_nekupps.pdf,

with 251 Kb.

See also the Leo Lundquist's M.Sc. thesis in Business available before in this website.

You can send an e-mail to MSc. Leo

Lundquist:

leo.lundquist@spray.se.

![]()

By M.Sc. Katia M.C. Rocha, Institute for Applied Economic Research - IPEA - from Brazilian Government.

This paper was presented in the Real

Options Conference at Chicago (September, 2000), and is based in a known

real options model for renewable resources, Morck & Schwartz &

Stangeland (1989), adapted to Amazon forest concessions.

This paper was presented in the Real

Options Conference at Chicago (September, 2000), and is based in a known

real options model for renewable resources, Morck & Schwartz &

Stangeland (1989), adapted to Amazon forest concessions.

Both paper (Word for Windows 97) and presentation (Powerpoint 97) both in

English are available to download. The files are compressed.

![]() To download the

Katia's paper on Amazon concessions,

click here (compressed file katia-amazon_paper.zip, with 170 KB).

To download the

Katia's paper on Amazon concessions,

click here (compressed file katia-amazon_paper.zip, with 170 KB).

![]() To download the

Katia's presentation on Amazon

concessions, click here (compressed file

katia-amazon_presentation.zip, with 709 KB).

To download the

Katia's presentation on Amazon

concessions, click here (compressed file

katia-amazon_presentation.zip, with 709 KB).

The Brazilian government is now planning to implement natural forest concessions for timber extraction. In addition to the legal requirements imposed on the management of concessions (minimum reserves, maximum extraction rates, etc.), the value of concessions is closely linked with uncertainties in estimates of the volume of commercial logs within the concession area and on future timber prices.

This paper proposes a method to appraise the value of forest concessions based on the real option theory (ROT). By combining the hypothesis of uncertainties in the volume of logs in a concession and future wood prices with inter-temporal maximization of profits, the method provides a more realistic estimate of the market value of concessions than does Net Present Value, which does not take these uncertainties into account.

Comparison between estimates using NPV and ROT shows that the latter are systematically higher. For the reference case, for example, the values using ROT are 140% higher. Since forest concessions are public resources, differences of that magnitude cannot be neglected. The paper also proposes methods to estimate the probability distribution of logging volumes in concession areas along with future prices. The volume distribution is specified in a spatial model as a function of geographic characteristics of the area as well of the neighboring areas.

You can send an e-mail to M.Sc. Katia

Rocha: katiaroc@iis.com.br.

By M.Sc. Jose Pablo Dapena, Finance Professor of Universidad del CEMA, Argentina

See the abstract below and download the paper (both in English).

Each company faces day to day investment opportunities. Just by staying in business the company is taking a decision of reinvesting. The question arising for those managers who have the responsibility of allocating capital is the criteria they should use to differentiate between investment alternatives. The most proven, traditional and popular method of valuation is Discounted Cash Flow (henceforth DCF), which provides comparable information. This method requires both the assessment of expected future cash flows and a risk adjusted rate (used in the discount coefficient).

Besides the current business the company is in, it can also face horizontal or vertical growth opportunities should events unfold favorable. Given the existence of these options for contingent or future growth, what would therefore be the value of the company?

![]() Download the

paper: the pdf file (Adobe Acrobat):

dapena-a_note.pdf, with 72 KB.

Download the

paper: the pdf file (Adobe Acrobat):

dapena-a_note.pdf, with 72 KB.

You can send an e-mail to M.Sc. Jose

Pablo Dapena: jd@cema.edu.ar.

By M.Sc. Ajax R.B. Moreira & M.Sc. Katia M.C. Rocha (Institute for Applied Economic Research - IPEA - from Brazilian Government) & Doctoral Candidate Pedro A.M-S. David (Furnas Centrais Elétricas)

See the abstract below and download the paper (both in English).

![]() Download the

pdf file (Adobe Acrobat) of this paper:

brazilian_investment_generation.pdf,

with 67 KB.

Download the

pdf file (Adobe Acrobat) of this paper:

brazilian_investment_generation.pdf,

with 67 KB.

The Brazilian Regulatory Framework for the Electricity Business was thoroughly to allow private investors to participate in the power generation, transmission and distribution. To be successful this policy shall provide attractive economical conditions for required investments in the system expansion, especially in new power generation. The Power Spot and Future Markets (forward contracts) are affected by the Regulatory Framework in many important aspects, such as:

The objectives of this study are:

You can send an e-mail to M.Sc. Katia

Rocha: katiaroc@iis.com.br.

By M.Sc. Katia M.C. Rocha & M.Sc. Ajax R.B. Moreira & M.Sc. Leonardo Carvalho & Ph.D. Eustáquio J. Reis, Institute for Applied Economic Research - IPEA - from Brazilian Government.

This is the second version of the paper on

real options value of a forest concession in Legal Amazon by the IPEA

researchers. The first version was presented in the Real Options

Conference at Chicago (September, 2000) and is available in this website

since then.

The second version was presented at the 5th Annual

International Conference on Real Options - Theory Meets Practice in

July 2001 at UCLA, Los Angeles. The new version has improvements like the

use of mean-reversion to model the timber prices, and more (both paper and

presentation in English).

This paper extend a known real options model for renewable resources,

Morck & Schwartz & Stangeland (1989), by using mean-reversion for

the timber prices and by considering the timber volume (biomass)

uncertainty, which is evaluated using spacial econometric tools. The model

was adapted to analyze the economic attractiveness of Amazon forest

concessions.

Both paper in .pdf (Adobe Acrobat) and the presentation (Powerpoint 97)

both in English are available to download. The files are compressed.

![]() To download the

paper on Amazon forest concessions, click

here (compressed file amazon.pdf with 108 KB).

To download the

paper on Amazon forest concessions, click

here (compressed file amazon.pdf with 108 KB).

![]() To download the

Katia's presentation on Amazon forest

concessions, click here (file Katia-ucla01.ppt, with 880 KB).

To download the

Katia's presentation on Amazon forest

concessions, click here (file Katia-ucla01.ppt, with 880 KB).

The Brazilian government currently implements concession policy to exploit timber harvesting on national forestry reserves in the Amazon region. This paper proposes methods to appraise the value of the forest concessions based upon option theory. Timber price is modeled as a mean-reverting stochastic process while the biomass volume follows the standard stochastic differential equation from the population ecology literature. Spatial regression estimates the probability distribution of biomass volumes in concession areas.

The concession value under option theory is 153% higher than the Net Present Value methodology. Since forest concessions are public resources, differences of that magnitude are not negligible.

You can send an e-mail to M.Sc. Katia

Rocha: katiaroc@iis.com.br.

By M.Sc. Juliana de Moraes Marreco, from the Universidade Federal de Minas Gerais (Belo Horizonte, Brazil), paper in Portuguese, abstract in English.

See the abstract below in English and download the paper (in Portuguese).

![]() Download the

pdf file (Adobe Acrobat) of this paper:

juliana-otimizacao_dinamica.pdf,

with 186 KB.

Download the

pdf file (Adobe Acrobat) of this paper:

juliana-otimizacao_dinamica.pdf,

with 186 KB.

This paper studies the option to abandon an offshore oil field. In other words, to answer the question: “when is it optimal to abandon an offshore oil fied, considering that future oil price is uncertain?” It is not just about abandoning the field when the operating costs become higher than the operating revenues. Uncertain can turn an unprofitable field into a highly profitable one, once there is an increase in oil prices. The model presented uses Dynamic Programming together with a non linear programming method (Golden Section Search) to calculate the critical values. The result is the boundary curve.

You can send an e-mail to M.Sc.

Juliana Marreco: juliana.marreco@uol.com.br.

By M.Sc. Jose Pablo Dapena Fernández, Finance Professor from Universidad del CEMA, Argentina

See the abstract below and download the paper (both in English).

Property in financial options (derivatives) is stated and transferred through contracts, while in real options property may arise from assets under the management of the firm, without a formal contract properly defining property. Furthermore, in some situations the asset can be public, and its property shared among different agents or firms. The present paper intends to work on the mechanisms of appropriation (and hence transferability) of real options exploring the assets that give rise to them, and proposing the concept of indirect property of complementary assets.

The meaning of property is explored, and also the dynamic of change between public and private assets. Finally, we develop on the features that define real options stemming from the indirect property of complementary assets.

![]() Download the

paper: the pdf file (Adobe Acrobat):

dapena-doc-trab_on_the_property_of_real_options.pdf,

with 64 KB.

Download the

paper: the pdf file (Adobe Acrobat):

dapena-doc-trab_on_the_property_of_real_options.pdf,

with 64 KB.

You can send an e-mail to Prof. Jose

Pablo Dapena: jd@cema.edu.ar.

Two articles presented in 2002 and 2003 at the 2nd and 3rd Encontro Brasileiro de Finanças ("Brazilian Finance Meeting"), both in Portuguese, by Elieber Mateus dos Santos and Edson de Oliveira Pamplona, from Universidade Federal de Itajubá.

The titles in Portuguese (English) are:

1) "Teoria das Opções Reais: Aplicação em Pesquisa e Desenvolvimento (P&D)" ("Theory of Real Options: Application in Research and Development (R&D)") and

2) "Qual o Valor de um Projeto de Pesquisa? Uma Comparação Entre os Métodos de Opções Reais, Árvore de Decisão e Vpl Tradicional na Determinação do Valor de um Projeto Real de Pesquisa e Desenvolvimento" ("What Is the Value of a Research Project? A Comparison Between Real Options, Decision Trees, and the traditional Npv to determination of the real research and development project value")

![]() Download the first paper (2nd EBF, 2002): the pdf file (Adobe Acrobat):

artelieber2oebf02.pdf,

with 170 KB.

Download the first paper (2nd EBF, 2002): the pdf file (Adobe Acrobat):

artelieber2oebf02.pdf,

with 170 KB.

![]() Download the second paper (3rd EBF, 2003): the pdf file (Adobe Acrobat):

artelieber3oebf03.pdf,

with 169 KB.

Download the second paper (3rd EBF, 2003): the pdf file (Adobe Acrobat):

artelieber3oebf03.pdf,

with 169 KB.

You can send an e-mail to MSc. Elieber

Mateus dos Santos:

eliebersantos@yahoo.com.br.

You can visit the Professor Pamplona Website.

![]()

This abstract is from a M.Sc. dissertation in Production Engineering, Financial and Investment Analysis concentration area, by PUC-RJ (Brazil). The authoress is Katia Maria Carlos Rocha

You can send an e-mail to Katia Rocha:

katiaroc@iis.com.br .

The model of her dissertation is the "time to build with technical

and economic uncertainties", analyzed in Dixit & Pindyck book and

in Pindyck (1993) paper. She follows one suggestion of Pindyck paper,

including an extension of the model (with two stochastic variables).

The major purpose of this dissertation is to develop rules for optimal

sequential investment decisions in presence of uncertainty and stochastic

control problems.

It presents three theoretical essays which apply the option pricing

theory approach to evaluate irreversible investments projects - Option

Pricing Theory in Real Assets.

The objectives are: evaluate the firm option to invest when it faces

uncertainty, establish the value of that option in each particular time,

and to find the optimal timing to invest, when the option should be

exercised.

Essays present investments projects which take time to complete or time

to build, and the firm faces with technical or financial constrains. These

investments projects are considered as sequential investments.

The use of numerical methods, as finite difference method, to solve

partial differential equations of parabolic and elliptic types raised by

the models, has to be mentioned as well as the free boundary problem.

As a practical tool, softwares are developed to simulate the models,

providing a rule for optimal sequential investment of each essay, as well

as many control simulations.

By M.Sc. Gunnar Kallberg and M.Sc. Peter Laurin, from Gothenburg School of Economics and Commercial Law, Department of Economics, Sweden.

You can send an e-mail to Gunnar

Kallberg:

gunnar.kallberg@mailbox.swipnet.se in order to comment or even

to request the full text dissertation and/or the Excel software from the

thesis.

Despite the wide use of the traditional capital budgeting techniques NPV, IRR, and Payback time among organizations, criticism have been raised against the static use of them. The techniques only use tangible factors and do not take into account intangible factors such as future competitive advantage, future opportunities, and managerial flexibility. A relatively new technique to capital budgeting is the real option approach. This approach has the potential to include the value of the project from active management and strategic interactions using the valuation technique for financial options.

The main objective of this thesis is to numerically analyze the value of an option approach in the capital budgeting of R&D investments. The results of the option approach will be compared with the results from traditional NPV approach. This will be done by constructing a valuation model and this model will then be numerically applied to a pharmaceutical R&D project at Pharmacia & Upjohn.

The model that we have constructed includes both the binomial and the Black & Scholes formula for the valuation of options. The binomial method is used in valuing the development phase of the R&D project and the Black & Scholes formula is used when valuing a follow-on project. A common spreadsheet program has been used to construct the model.

The case study showed that the option valuation approach gave a similar result as the traditional NPV when applied to the R&D project at Pharmacia & Upjohn. The reason why the two methods gave similar results were because the expected cash inflows were high in comparison to the investment costs. Therefore, the abandonment value in the development phase had almost no value and hence, did not give any extra value to the project. The value of the follow-on project valued as a growth option gave a higher value than the NPV approach and hence, a higher total project value. A sensitivity analysis of the project showed that the option approach became increasingly valuable when the expected cash inflows decreased.

The model shows that a user-friendly spreadsheet including an option approach could be a valuable and descriptive tool to add to a traditional NPV technique. The conclusion of the thesis is that Pharmaciy & Upjohn should consider implementing the real options approach in order to value the flexibility and opportunities inherent in their future projects.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}